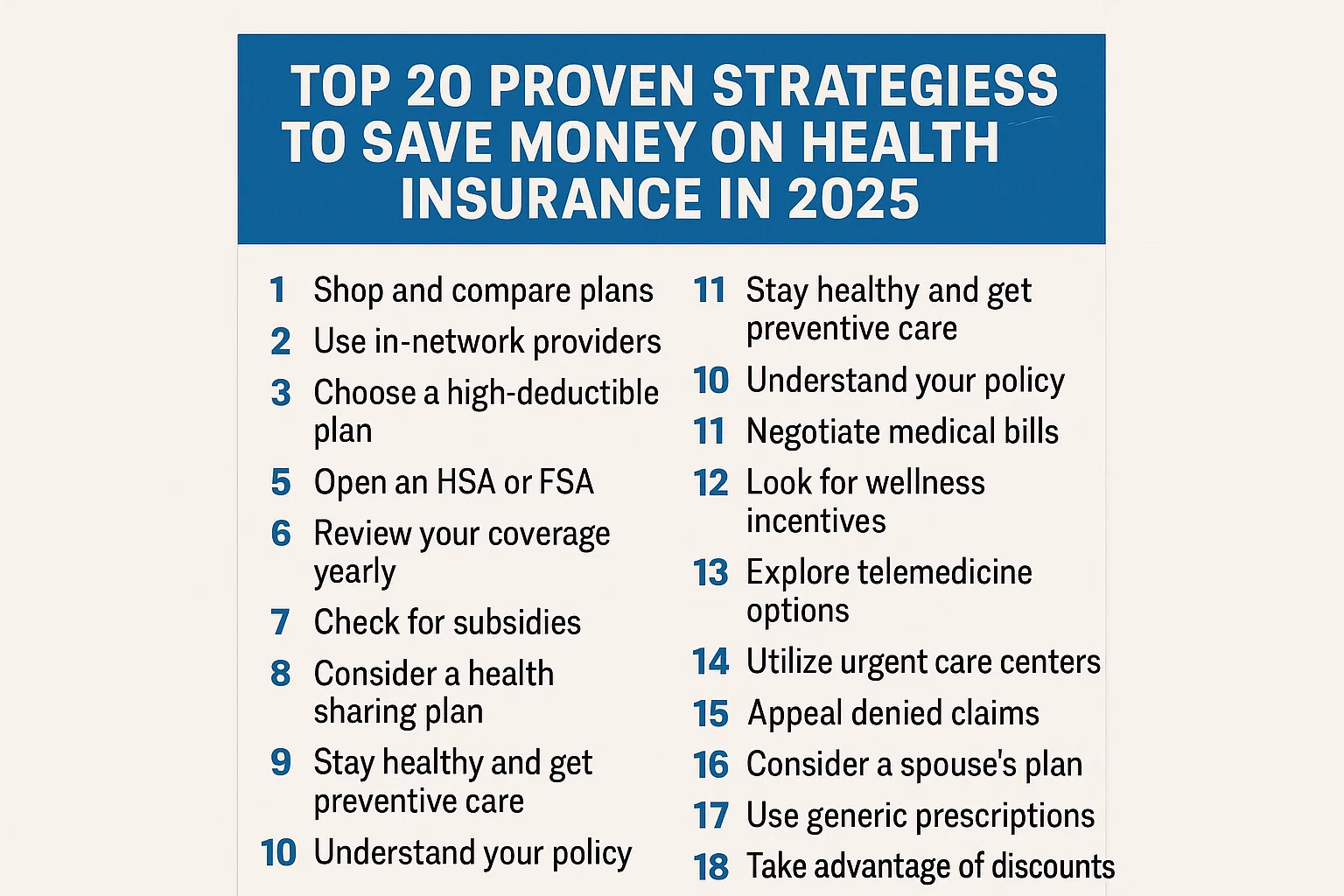

Top 20 Proven Strategies to Save Money on Health Insurance in 2025

Introduction

Health insurance has become one of the most significant expenses for families and individuals worldwide. In 2025, premiums, deductibles, and out-of-pocket costs are expected to continue rising, making it critical to find effective strategies to reduce costs. Whether you are self-employed, employed, or managing family coverage, saving on health insurance requires knowledge, smart planning, and awareness of global opportunities. This blog covers 20 proven strategies to save money on health insurance without sacrificing the quality of coverage.

1. Compare Multiple Health Insurance Plans Annually

One of the biggest mistakes people make is sticking with the same insurer year after year. By comparing plans annually, you can identify cheaper premiums, better networks, or enhanced benefits. Platforms like Healthcare.gov (U.S.), Policybazaar (India), or ComparetheMarket (U.K.) provide side-by-side comparisons to ensure you don’t overpay.

2. Take Advantage of Employer-Sponsored Health Insurance

If you are employed, always evaluate your company’s health insurance benefits. Many employers cover a significant portion of the premium. You might also have access to flexible spending accounts (FSAs) or health savings accounts (HSAs) to reduce taxable income while paying medical costs.

3. Open a Health Savings Account (HSA)

An HSA is one of the most powerful tools to save money. Contributions are tax-deductible, grow tax-free, and can be withdrawn tax-free for medical expenses. In 2025, the contribution limits have increased, making HSAs even more attractive for high-deductible health plan (HDHP) holders.

4. Explore Government Subsidies and Tax Credits

Many countries provide subsidies for lower and middle-income households. For example, the Affordable Care Act (ACA) in the U.S. offers premium tax credits, while the U.K. has NHS support options. Always check eligibility annually, as income and policy changes affect your qualification.

5. Bundle Insurance Policies

Bundling health insurance with life or auto policies can sometimes reduce premiums. Some insurers reward customers with loyalty discounts when multiple policies are purchased together.

6. Focus on Preventive Care

Preventive care, such as annual checkups, screenings, and vaccinations, is usually covered at no cost. By focusing on preventive health, you can avoid costly treatments for conditions detected late.

7. Choose Generic Prescription Drugs

Always ask your doctor if a generic version of your medication is available. Generics can cost up to 80% less than branded drugs, saving thousands per year.

8. Use Telemedicine Services

Telemedicine is cheaper than in-person visits and is increasingly covered by insurers worldwide. Virtual consultations can save time, travel costs, and reduce unnecessary ER visits.

9. Negotiate Medical Bills

Few people realize that medical bills are negotiable. Hospitals often provide discounts for upfront payments or financial hardship. Always request an itemized bill and question charges that seem excessive.

10. Join Health Insurance Cooperatives

Health sharing ministries and cooperatives allow members to pool resources and share medical expenses. While not traditional insurance, these can be significantly cheaper options for healthy individuals.

11. Consider High-Deductible Health Plans (HDHPs)

HDHPs offer lower monthly premiums but higher deductibles. If you are generally healthy and rarely visit doctors, an HDHP combined with an HSA can save substantial money.

12. Review Your Coverage Needs

Avoid over-insuring. For example, single individuals may not need maternity coverage. Customizing your policy to exclude unnecessary features can cut premiums by 20-30%.

13. Stay In-Network

Always use doctors and hospitals within your insurer’s network to avoid surprise bills. Out-of-network costs can be several times higher than in-network rates.

14. Maintain a Healthy Lifestyle

Insurers often offer discounts for healthy policyholders. Non-smokers, active individuals, and those with good BMI scores often qualify for wellness incentives and lower premiums.

15. Use Preventive Dental & Vision Coverage

Dental cleanings and eye exams can detect health issues early. Bundling dental and vision with health insurance may save you money in the long run by preventing costly treatments.

16. Check for Corporate Wellness Programs

Many employers provide wellness programs, gym reimbursements, and even free therapy sessions. Taking advantage of these programs can reduce medical claims and lower future premiums.

17. Opt for Annual Payments

Some insurers provide discounts if you pay your premium annually instead of monthly. This can save 3–5% per year.

18. Explore International Health Insurance Plans

If you live abroad or travel frequently, international health insurance providers (like Cigna Global, Allianz, and IMG) may offer cheaper coverage with better global access compared to local insurers.

19. Use Tax-Advantaged Accounts

Aside from HSAs, some countries offer tax relief for medical expenses. For example, in India, Section 80D of the Income Tax Act allows deductions for health insurance premiums.

20. Reevaluate Insurance Annually

Life circumstances change — marriage, children, career shifts, or relocation can all impact your health insurance needs. Always reassess coverage annually to avoid overpaying.

Conclusion

Health insurance costs continue to rise worldwide, but with proactive planning, awareness of government programs, and strategic use of tax-advantaged accounts, individuals and families can save thousands annually. The key is to compare, negotiate, and stay updated on new opportunities. By applying the 20 strategies outlined in this blog, you can ensure financial security while accessing quality healthcare in 2025 and beyond.

Comments (3)